How to Make Sense of Your CIBIL Report and Improve Your Credit Score

What is a CIBIL Report?

A CIBIL report is a comprehensive document that provides a detailed overview of your credit history. It’s generated by the Credit Information Bureau of India Limited (CIBIL), one of India’s most trusted credit information agencies. This report includes your personal information, credit accounts, loan details, and payment history.

The centerpiece of your CIBIL report is the CIBIL score, a three-digit number ranging from 300 to 900. This score is a quick snapshot of your creditworthiness, with higher scores indicating better credit health.

Learn more about credit reports from the Reserve Bank of

Your CIBIL score plays a crucial role in your financial life. Here’s why it matters:

-

- Loan Approval: A high CIBIL score increases your chances of loan approval.

-

- Interest Rates: Lenders often offer lower interest rates to individuals with higher scores.

-

- Credit Limits: A good score can help you secure higher credit limits.

-

- Negotiating Power: With a high score, you’re in a better position to negotiate loan terms.

-

- Financial Credibility: Your score reflects your financial responsibility to potential lenders.

How is Your CIBIL Score Calculated?

CIBIL collects and maintains credit-related information from various lending institutions on a monthly basis. They use this data to generate your Credit Information Report (CIR) and CIBIL score. The score is calculated based on several factors:

-

- Payment History (35%)

-

- Credit Utilization (30%)

-

- Length of Credit History (15%)

-

- Types of Credit (10%)

-

- Recent Credit Inquiries (10%)

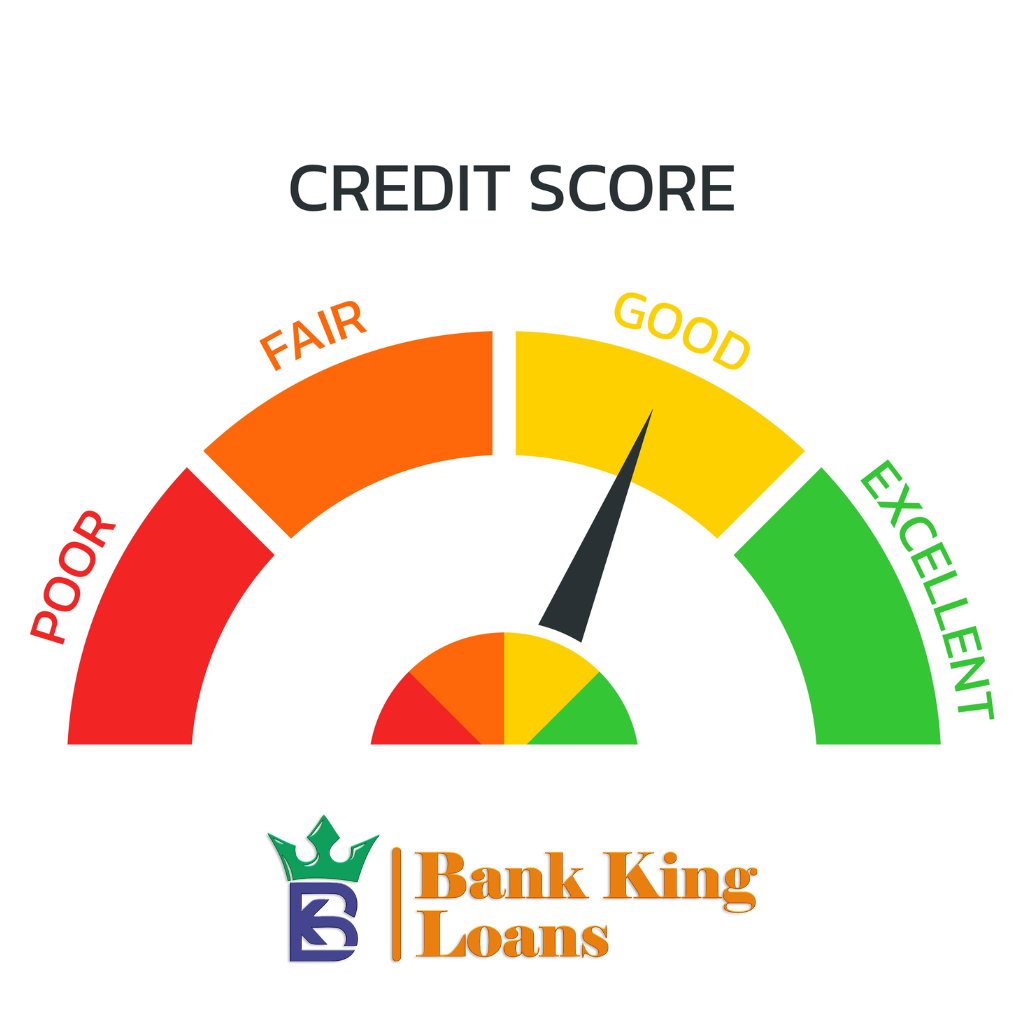

UNDERSTANDING Your CIBIL Score

Understanding what your CIBIL score means can help you gauge your financial health:

| Score Range | Category | Significance |

|---|---|---|

| Below 300 | Poor | No credit history – unable to assess creditworthiness |

| 300 – 550 | Very Low | Potential credit issues – improvement needed |

| 551 – 620 | Low | Improvement required for better loan terms |

| 621 – 700 | Fair | Close to good – constant monitoring needed |

| 701 – 749 | Good | Committed credit conduct – eligible for favorable terms |

| 750 – 900 | Excellent | Sound credit behavior – best loan offers available |

The ideal credit score for most personal or business loans is above 750. However, for secured loans like home loans, lenders may accept slightly lower scores.

Tips to Improve Your CIBIL Score

If you’re looking to boost your CIBIL score, consider these strategies:

-

- Pay EMIs on Time: Consistent, timely payments are crucial for a good credit record.

-

- Maintain Low Credit Utilization: Keep your credit card balances well below the limit.

-

- Avoid Unnecessary Credit Applications: Don’t apply for credit facilities you don’t need.

-

- Manage Credit Cards Wisely: Limit yourself to one or two active credit cards.

-

- Cancel Dormant Cards: Close credit cards you no longer use.

-

- Space Out Loan Applications: Avoid making multiple loan applications in quick succession.

-

- Be Cautious About Co-signing: Think twice before becoming a co-signer on a loan.

Check out these additional tips from the National Stock Exchange of India

Common Misconceptions About CIBIL Reports

Let’s clear up some common misunderstandings about CIBIL reports:

-

- Myth: You need to carry a balance on credit cards to build credit. Fact: Paying your full balance each month is the best practice for your credit score.

Getting a Loan with a Poor Credit Score

While a good CIBIL score is preferable, all is not lost if you have a poor score. Here are some options:

-

- Non-Banking Financial Companies (NBFCs): Some NBFCs are more flexible with credit scores, though they might charge higher interest rates.

-

- Secured Loans: Offering collateral can increase your chances of approval, as it reduces the lender’s risk.

- Co-signer or Guarantor: Having someone with a better credit score co-sign your loan can improve your chances of approval.

Frequently Asked Questions

-

- Q: How often is my CIBIL report updated? A: CIBIL reports are typically updated monthly as lenders report new information.

-

- Q: Can I get my CIBIL report for free? A: Yes, you’re entitled to one free CIBIL report per year. You can request it from the CIBIL website.

-

- Q: How long does negative information stay on my CIBIL report? A: Most negative information remains on your report for 7 years.

-

- Q: Can I dispute errors on my CIBIL report? A: Yes, you can file a dispute with CIBIL if you find any inaccuracies in your report.

-

- Q: Does my income affect my CIBIL score? A: Your income doesn’t directly affect your CIBIL score, but it may influence your credit limits and loan approvals.

Understanding your CIBIL report is a crucial step towards financial health. By regularly monitoring your report, addressing any issues, and maintaining good credit habits, you can work towards a strong CIBIL score that opens doors to better financial opportunities.

Remember, your CIBIL score is not set in stone. With consistent effort and responsible credit behavior, you can improve your score over time. Start today by checking your CIBIL report and taking steps to boost your creditworthiness.